How Far Can Rates Rise In Australia?

All the talk in recent times has been around interest rates and exactly just how far the RBA could potentially go when they eventually start their tightening cycle, and how quickly this will occur.

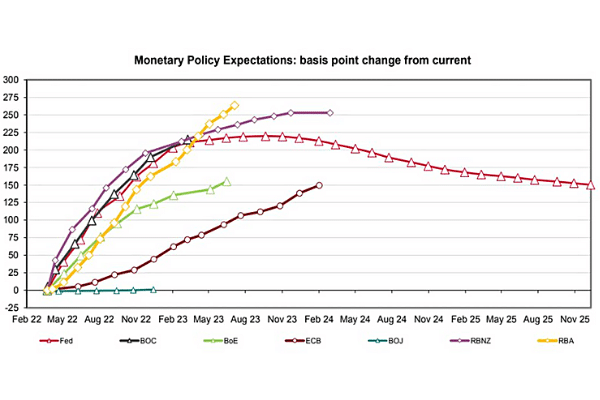

While we all understand that interest rates need to move back to a more balanced level than what we’ve been experiencing, notably, the market is predicting that not only will rates rise, but the RBA will take the cash rate higher and faster than most of the other major world economies.

The latest projections compiled by Westpac, see the cash rate starting to rise mid-year with a string of hikes that would push the OCR to around 2.65 per cent.

The first interesting point to note is the expectation suggests the RBA will hike to a level greater than the FOMC. Currently, the US Federal Reserve is just starting to battle record high inflation that is sitting at 7.9 per cent – the highest in 40 years.

Meanwhile, the market expects the RBA to move beyond the Fed, to tackle inflation in Australia that is currently less than half that at 3.5 per cent.

There are also other key differences in the way the RBA and Fed operate. The Federal Reserve clearly pays close attention to the state of the US stock market and is loath to act in a way that causes a major dislocation that might push the economy into recession. However, Chairman Powell is now communicating that they will act aggressively and quickly to normalise rates as rapidly as possible.

In Australia, there is far more emphasis on the residential property sector which is our largest asset class by far and the RBA does not want to act in a way that destabilises this so as to avoid the flow-on effects which could result in a recession. The real estate sector provides a very large portion of both direct and related employment within the Australian economy and is vitally important in assisting overall consumer sentiment, spending and wages growth.

It’s for those reasons I think the true terminal cash rate in Australia is likely to end up lower than what the market is currently predicting.

If the cash rate rose to 3 to 3.5 per cent, that would put pressure on housing prices which in turn would mean the banks may lose a substantial portion of their normal mortgage buffer – based on a typical 80 per cent loan to value ratio for retail borrowers. This would obviously cause some negative issues in relation to the financial stability of the Australian banking system and is thus a matter of great importance for the RBA.

The other important consideration is that the RBA is likely to quickly adjust to what might happen after just a few initial interest rate increases. As we know, sentiment impacts all markets and can be a very powerful force. If these interest rate rises slow down consumer spending and cap some of the hotter housing markets, that might be enough to moderate inflation and bring it back to the RBA’s target band of 2-3 per cent. I think the more important issue is for the government to assist in bringing more skilled and unskilled labour into Australia via targeted international immigration initiatives so that some of the supply constraints that impact current inflation pressures are sustainably eased for the longer term.

The RBA will try to remain more patient than the FED, because it can, and not tip the economy into recession when it really doesn’t need to based on the current levels of inflation. They will change course as required and adapt to the new data as it presents itself.

While the Fed should act more aggressively at this point in time, the RBA doesn’t yet have to and that could mean they might not even raise rates by 25 basis points until August while markets are now predicting a June rate increase.

We do have a Federal Election approaching rapidly and the opinion polls favour a change of the guard to Labor, but a focus on full employment will likely remain regardless of a change of government. RBA Governor Lowe continues to prioritise this against the market pressures to lift interest rates. He sees sustainability as a key consideration, so inflation must be sustainably within the RBA’s target range of 2-3% before a rate rise is on the table.

The other wildcard for the RBA which differs from the Fed is the impact of commodity prices on the AUD. I recently spoke about how I felt the AUD/USD needed to appreciate thanks to the rise in commodity prices that we have witnessed over the last few months and so far, that’s what we’ve been seeing with the Aussie hitting 75 cents against the USD last week.

With the war in Ukraine also likely to see more ongoing strength in demand for a range of commodities which Australia supplies, that’s going to mean that the AUD could see more ongoing upward pressure which helps the RBA tackle consumer-driven inflation as a tailwind

Meanwhile, the Aussie banks have been raising their fixed rates virtually weekly for a number of months based on their cost of funding. The bond markets could well be getting ahead of themselves with the trajectory of the shorter-term increases being a bit too steep at this stage.

Given the amount of household debt that exists, I suspect the terminal cash rate should end up around 1.75 – 2.25 per cent, which is less than the market predicts and approximately what we are hearing from many economists. At this point in time, the market projections are simply not in keeping with the current conditions. The danger remains that rates increase too much and trigger a recession; however, I don’t see this as being the base case.

As they always do, the central bankers will continue to adjust their predictions as more data becomes available, but for the time being, I can’t see rates rising to the levels markets are predicting over such a short time frame.