The Ups and Downs of Sydney’s House Price Cycle

Anyone who has been in real estate long enough understands that property is cyclical in nature. There are periods of strong growth, followed by lengths of time where prices either stagnate or fall.

But over the long run, prices continue to rise, and this has been a great builder of wealth for many Australians.

Now that interest rates have begun to rise, the market has returned to a far more normal setting. Over the past few years, we’ve seen incredibly low inventory levels, and with demand surging from record low-interest rates and a host of incentives, it’s certainly been a seller’s market.

Now that the heat has started to come off, it’s worth taking a look at how this last cycle has played out in a historical context and what might be in store for the months ahead.

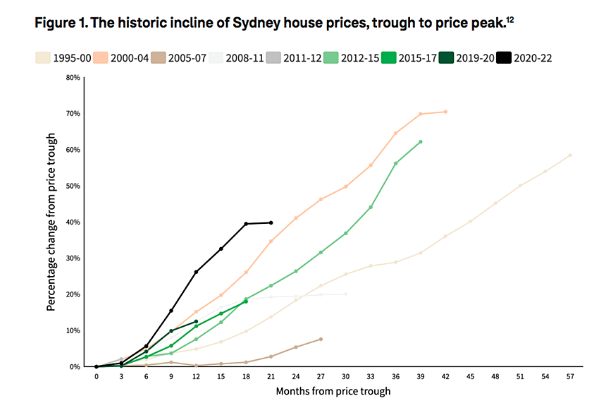

According to Domain’s New South Wales Spotlight Report, we can see that the last up-move in property values across the state has been as sharp as we’ve ever seen before.

House prices rose 40% in under two years – a massive rise in a short period of time. That’s a median daily increase of $708 throughout the pandemic. Technically, previous upswings have seen greater rates of house price growth over a longer period of time. However, the most recent one provided the quickest and sharpest equity boost Sydney property has ever experienced – a great time for homeowners and investors alike.

Sydney’s housing market is now technically entering into a downturn with many market indicators weakening despite overall house prices nudging marginally higher during the first quarter of 2022 according to Domain. The latest data from CoreLogic shows that Sydney dwelling values fell by 2.8% over the June Quarter.

Across the various segments of the market, the premium price-point is leading the price cycle direction as 6.5% was shaved from house prices over the first quarter of 2022.

The report has noted that the most expensive areas of Sydney in the Eastern Suburbs have seen the median house price falling 8.5% since its peak in June-2021, and it was the first Sydney region to hit a price peak. It is worth noting that CoreLogic’s stratified hedonic dwellings index (3 months to March) showed only a 0.2% decline for the highest 25% value segment, and the June quarter declined by 4.3%, which supports the trend that is developing.

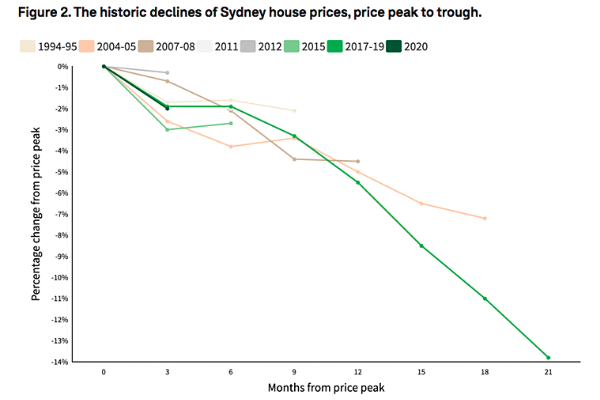

While prices have been easing in some areas, Domain also notes that historically downturns have been shorter and less severe compared to the preceding upswing.

There is often a greater percentage increase in price relative to the subsequent decline, so it is unlikely we will see a return to pre-pandemic prices. I believe this data may vary considerably between the various capital city and regional markets and we will examine this further in our upcoming online quarterly review in August.

The report said that the last significant downturn was during 2017-19 when Sydney house prices fell 13.8% from peak to trough.

This price decline was not due to rising interest rates or recessionary pressures, but the intervention of regulators such as APRA and subsequent bank policy changes which made it far more difficult for people to obtain loans and less total credit being available for borrowers, plus the negative effects of the banking royal commission to add to this financially induced downturn.

Although interest rates are important, they are not the only factor influencing housing prices with taxes, banking regulation, population and income growth, and the responsiveness of new housing supply to growing demand are all drivers of property prices.

While falling interest rates have been a key driver of rising house prices in Australia and across the world the higher level of debt means that the RBA shouldn’t need to increase rates as much as it has in the past to cool demand-driven inflation.

It’s also worth noting that while the state as a whole has seen strong growth when we break down the areas that have seen the largest gains, they are very diverse.

Some homeowners in areas such as Terrigal on the Central Coast and Palm Beach on the Northern Beaches saw prices rise by over 50% over the past 12 months alone. While other areas have seen far lower levels of growth.

Like anything in property, we can’t simply buy properties based on broad-based figures.

While the market is cooling from the record-setting pace that we’ve experienced over the past two years, the numbers show us that not all locations are equal.

There will still be many opportunities ahead, but it’s more important than ever that you identify high-quality assets in locations where demand will remain strong over the medium to long term.