Property vs. Shares – The Age Old Dilemma

“Should I invest in property or should I invest in shares..?” – A question that has puzzled investors across the globe for decades…and will likely continue to do so.

There is no short answer to this broad question, so we’ve presented an unbiased view of each option below in our Property vs. Shares post with regard to some key features we look for when investing.

Risk and Return

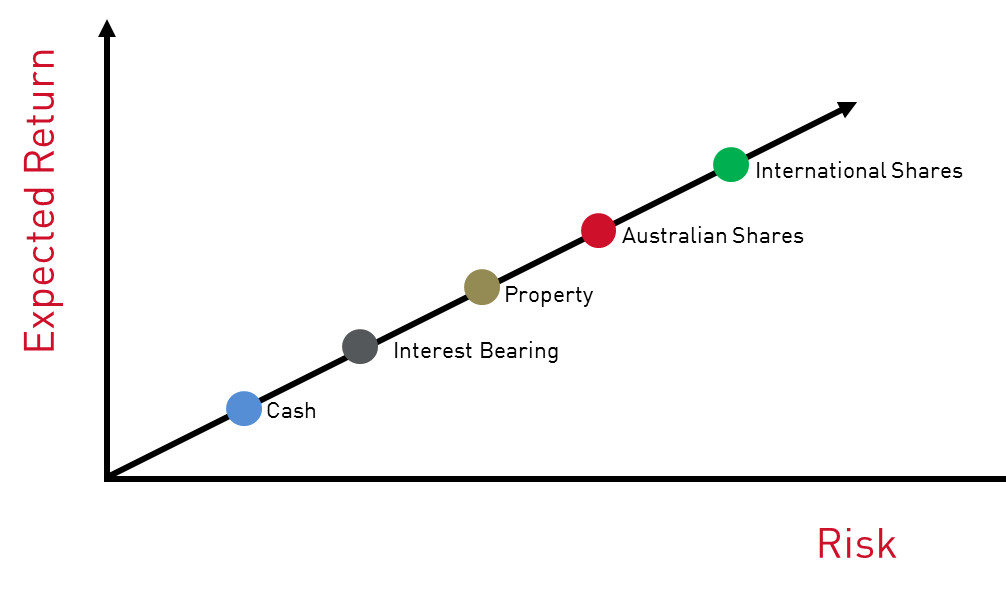

As most investors will know, risk is positively correlated with return. As we take on greater risk, we typically do so with the expectation of a higher return on our investment. Property is regarded as having both a lower risk and expected return compared to shares, as reflected in the graph below:

However, does this relationship hold true in reality…

When we look at the last 20 years in Australia, residential property outperformed shares earning an annual return of 9.9%, compared to just 8.7% in shares.

When we look further back, all the way to 1926, we see a similar return generated between the two, with shares delivering 11.5% per year and residential property delivering 11.1% per year. The two have therefore delivered similar returns to investors over time.

Transparency

An investment property offers much greater transparency, given that the investor can physically inspect the property, and employ the expertise of those experienced in the sector to carry out these inspections on their behalf. This is in contrast to shares, which is reliant on the directors fully disclosing all relevant information to shareholders as well as shareholder protection laws being adequate across various jurisdictions.

Size of the Market

The size of the residential property market in Australia is much larger than that of the stock market. The property market is estimated at over $5 trillion, while the market capitalisation of the Australian Stock Exchange is closer to $1.5 trillion, less than 1/3 of the size of the residential property market.

Upfront Costs

Property transactions have much higher upfront costs to be considered than purchasing shares including stamp duty, registration fees, deposits, inspections etc. This therefore results in property investment typically being a longer-term strategy.

Using Leverage

Most people who have utilised margin lending when it comes to investing in shares have likely had the negative experience of a margin call. This is a situation whereby your lender calls you requesting that you ‘top up’ your investment account with cash within a matter of days because the value of your shares has fallen. This is often a dangerous strategy and can result in many sleepless nights.

Given that property is not a ‘mark-to-market’ asset, the bank generally does not call requesting more capital if the value of it drops. As long as you continue to make your interest repayments, the bank is happy for the value of your property to fluctuate and you can remain focused on your long-term wealth creation. This provides peace of mind and a much more sound strategy when it comes to utilising leverage.

To put this into context, you may borrow 80% to invest in a $600,000 property in Australia or you could borrow 80% to invest in a portfolio of shares. It would be a relatively safe bet to assume that the property investment would be the strategy that remains in place and generates a long-term positive return.

Security

‘Safe as houses’ – we often hear this phrase and there is certainly a reasonable amount of truth to it. This high level of confidence continues to encourage people across the globe to invest large amounts of capital in property. This is also represented by the banks in Australia who will lend 80 – 85% against investment properties, which compares generally to 50% against shares.

Property is generally more likely to have some intrinsic value when compared to shares also. It is therefore less likely to result in a complete loss of capital.

Property vs. Shares…so what is the answer..?

The simple answer is DIVERSIFICATION

Crunch your numbers with the help of a professional Adviser and define your wealth creation or consolidation strategy that will allow you to achieve your financial goals. This may involve a combination of investing in property, shares and bonds. It is important that you’re clear on the role that each will play in your own journey towards financial freedom.

To your investing success!

Related Tags: Property Investment in Australia | Australian Property Investment