Should Investors be Worried about Rental Yield Compression?

The Holy Grail for most property investors is normally a combination of capital growth and strong rental yield.

Recently, we’ve seen a very clear shift towards capital growth. Looking at the latest data from CoreLogic and it’s clear that property prices are increasing rapidly, with dwelling values up by 18.4% around the country in the past 12 months.

The net effect of this surge in house prices is that rental yields (annual rental income/property value) have fallen away or compressed.

After initially suffering a sharp decline in rents with the onset of lockdowns in 2020, we are starting to see upward pressure on rents in many areas of Australia. Nationally, rents have lifted by 8.2% over the 12 months ending August, the largest rise in rents since 2008.

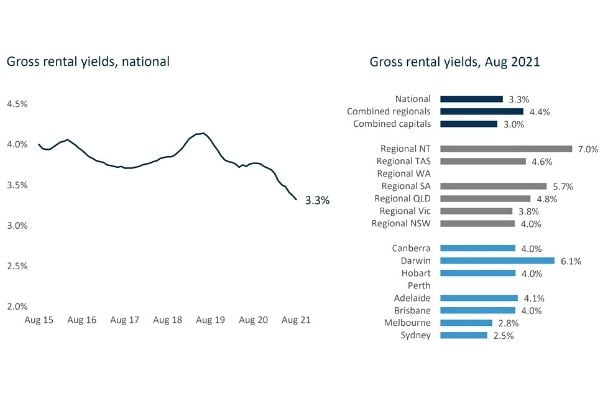

With national housing values rising by 18.4% and rents rising by a lower 8.2%, the result is ongoing yield compression.

Nationally, gross rental yields have fallen to an all-time low of 3.32%. It is no longer just Sydney and Melbourne where rental yields are sitting at historic lows. Brisbane (3.99%), Hobart (4.01%) and Canberra (3.99%) have also seen gross rental yields fall to new record lows in August.

New investors can at times get confused or concerned by the fact that rental yields are falling. On the surface, falling yields potentially make it more difficult to hold a property. The flip side of this is that yields are only falling because the underlying asset is growing so quickly. This is the same way bonds move, with the yield being inversely related to the price.

One of the key drivers of house prices has been the sharp cuts to interest rates from the RBA that have made borrowing money as cheap as it’s ever been before.

In the current environment, you can borrow $1 million and you’ll only be paying back around $400 per week in interest (2.0% interest rate). These are the kind of borrowing rates that we’ve not seen in over 50 years and make houses more affordable to own than rent in many parts of Australia. And it’s seeing a surge in people looking to invest in property. Both for the yield on offer and the capital growth potential.

Impact on Investors

The most important thing for investors to take into consideration when looking at rental yields compressing is the net impact of what is going on with increasing house prices values.

For example, if you purchased a $1 million property 12 months ago, you may have seen that property grows in value to approximately $1.2 million depending on where it is located.

While the rental yield itself might now have fallen from 5% to 4%, the net impact to an investor is that you’ve seen a significant increase in your equity.

While interest rates remain low, the biggest risk to an investor is waiting too long and missing out on current borrowing possibilities that may not exist in the future.

While property prices are moving higher, it’s important to capitalise on that growth. In another 12 months time, it’s likely that property prices will be higher than they are now and yields will also be lower.

Impact of Interest Rates

In the current low-rate environment, it’s also prudent to consider what might happen with interest rates in the future and take some steps to provide some “peace of mind”.

RBA Governor Lowe has made it very clear that the board won’t be acting quickly to lift rates and when they do, any moves will be slow and steady. It’s also worth looking at the impact of yields in a rising interest rate environment.

If interest rates do move, it’s normally because the economy is overheating and inflation is creeping up. Rising inflation can be positive for house prices.

It also means that with higher house prices, there will be borrowing constraints which will lead many would-be homeowners to have to stay as renters. This, in turn, puts added pressure on rents and lifts yields.

The most important consideration if you have been considering buying a new home, or investment property in the current environment, is to act sooner rather than later while property prices continue to trend higher. You want to be a buyer while prices are moving up.

It is always important to note that research is very important as many of the reported statistics are quite generic. A good example of this would be what has happened with rental yields in inner-city lower quality apartments in Melbourne, as opposed to large, high-quality ones which have been designed for owner-occupiers and are located in the inner-middle ring.

That way, yield compression can work in your favour and not against you.